Fortis (TSE:FTS) Stock is Finally Soaring – Is It Worth a Buy Still?

Fortis: Strong Q2 Earnings But Is the Stock Overvalued?

Fortis Inc. (NYSE: FTS) is an electric and gas utility company, operating across Canada, the United States, and the Caribbean, and is a prominent player in North America’s regulated utility sector. Since its founding in 1987 with assets of just $390 million, Fortis has expanded its asset base to $69 billion, driven by strategic growth and diversification.

In this analysis, we review Fortis’ recent Q2 earnings results, explore Wall Street’s views, conduct a fair value assessment, and analyze options market sentiment to assess whether Fortis presents a compelling investment opportunity.

Earnings Recap

On July 31, Fortis announced its Q2 2024 earnings, reporting an EPS of $0.67, which surpassed Street expectations of $0.47. This strong performance reflects the stability of its regulated utility businesses, which continue to deliver solid results despite broader industry challenges.

According to CEO David Hutchens, Fortis is making steady progress on its $4.8 billion capital plan for 2024 and remains committed to its five-year, $25 billion investment strategy.

These investments aim to enhance infrastructure, improve grid resilience, and support the transition to cleaner energy sources. Additionally, Fortis released its 2024 Sustainability Report, highlighting key achievements in reducing emissions and promoting sustainability.

With a projected annual rate base growth of 6.3% through 2028, Fortis expects to maintain its 4%–6% annual dividend growth target, reinforcing its long-term value proposition for shareholders.

Analysts’ Views

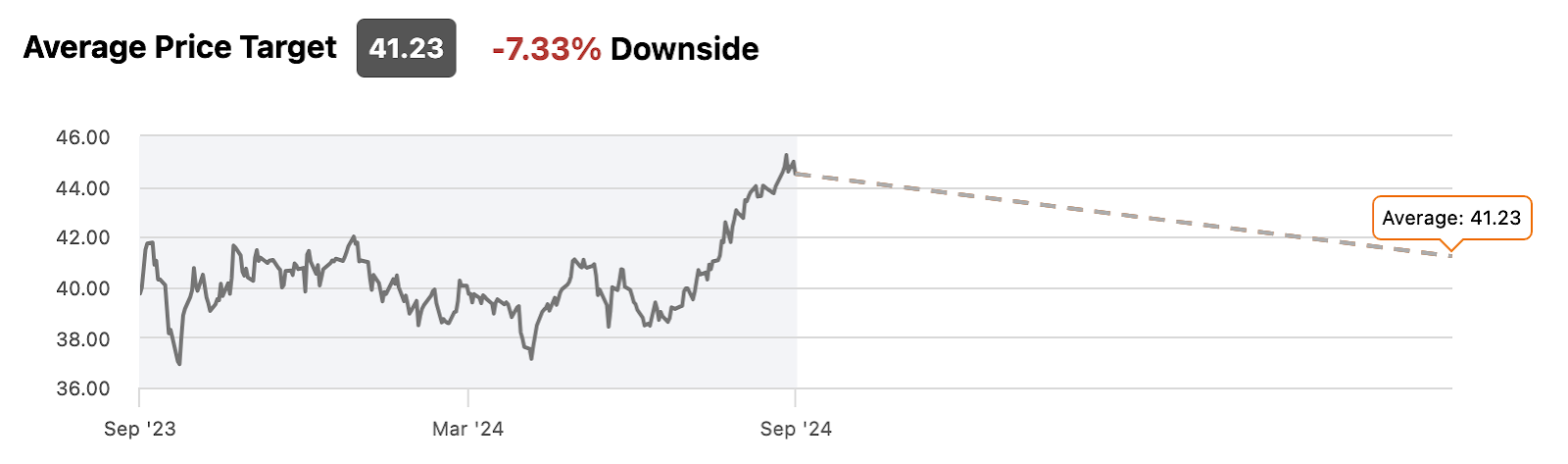

Wall Street analysts are generally neutral on Fortis, with an average “Hold” rating. Price targets range from $29 to $46, with an average target of $41.23, indicating a potential downside of about 7% from the current stock price.

Source: Seeking Alpha

What Bulls Are Saying about Fortis

Fortis is expected to see positive EPS growth, with forecasts reaching $3.32 in 2024 and $3.46 in 2025. This is largely driven by favorable foreign exchange impacts and improvements in the allowed return on equity at its Central Hudson subsidiary.

The company’s ambitious $25 billion capital investment plan is projected to boost rate base growth and future cash flows. These factors suggest a stable outlook for long-term investors looking for steady returns.

What Bears Are Saying about Fortis

However, the company has faced setbacks, particularly in Central Hudson, where higher-than-expected operating costs and regulatory challenges have dampened earnings. Fortis is also exposed to risks such as declining electricity and gas demand, regulatory pressures, and adverse economic conditions in its service areas, all of which could affect its earnings growth.

Operational challenges in newly acquired businesses further exacerbate concerns, creating uncertainty about the company’s ability to maintain investor confidence.

Fair Value Assessment

Based on our detailed valuation analysis using multiple models such as the Dividend Discount Model (DDM), EV/EBITDA, and price-to-earnings ratios, our estimate places Fortis’ fair value at approximately $35 per share. This indicates a potential downside of around 21% from its current price, suggesting that the stock is overvalued and more bearish than Wall Street’s current consensus.

Options Market Sentiment

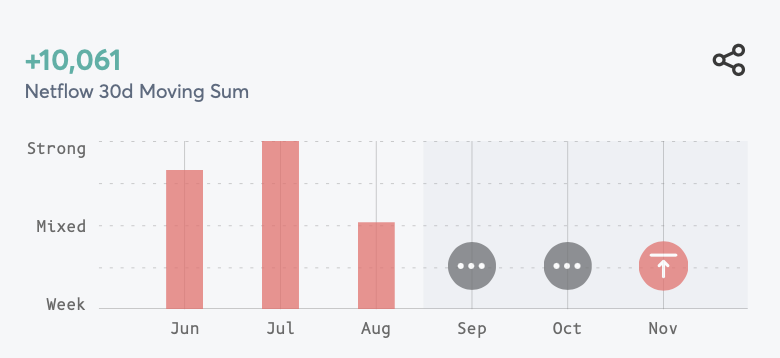

The options market also reflects uncertainty. A +10,061 netflow 30d moving sum shows slight buying interest, but with mixed predictions for September and October, indicating volatility without a clear direction. By November, the stock is expected to face a resistance test, where it may struggle to break through key price levels, further complicating its outlook.

Source: Visual Sectors

Conclusion

Fortis posted strong earnings in Q2, but analysts remain cautious, with price targets suggesting overvaluation. Our fair value assessment is even more bearish, implying that the stock is significantly overpriced. Coupled with mixed sentiment in the options market, we recommend selling Fortis, as there appears to be limited upside potential in the near term.