Is Brookfield Corporation (TSE:BN) Still a Buy After Touching All-Time Highs?

Brookfield Hits 52-Week High: Strong Earnings, Analyst Optimism, but Is the Stock Overvalued

Brookfield Corporation (NYSE: BN) is a prominent alternative asset manager, specializing in real estate, renewable power, infrastructure, private equity, and venture capital investments. The firm provides a wide range of public and private investment products and services to institutional and retail clients globally.

At the end of August, Brookfield’s stock soared to a 52-week high, riding on bullish investor sentiment driven by the company’s strategic investments and asset management activities. Brookfield has experienced substantial stock growth, with shares up approximately 18% year-to-date.

In this review, we will delve into Brookfield’s recent earnings, evaluate Wall Street analysts’ perspectives, and provide a fair value assessment to determine if now is the right time to invest in Brookfield and whether there’s more upside potential.

Recent Earnings Review

Brookfield reported solid second-quarter results on August 8, with an EPS of $1.35, surpassing the analyst estimate of $0.77. Although revenue came in slightly below expectations at $1.24 billion (versus the consensus estimate of $1.26 billion), the company’s overall performance remained impressive.

Brookfield posted an 11% year-over-year increase in distributable earnings before realizations, reaching $1.1 billion for the quarter. Even more noteworthy, total distributable earnings soared by 80%, totaling $2.1 billion, fueled by favorable economic conditions and liquidity in private markets. These earnings gains are expected to drive future growth.

Brookfield has strategically invested in sectors like renewable energy and data centers, positioning itself to capitalize on trends related to artificial intelligence and technology infrastructure. In the past six months, the company financed $75 billion in debt and realized $15 billion from asset monetizations, underscoring its efficient capital management.

Brookfield’s forward-looking strategy includes ramping up fundraising efforts and increasing transaction activity to enhance its performance in the coming quarters. Furthermore, the company has a robust operating and development pipeline exceeding 230 gigawatts, which is expected to contribute to long-term earnings growth.

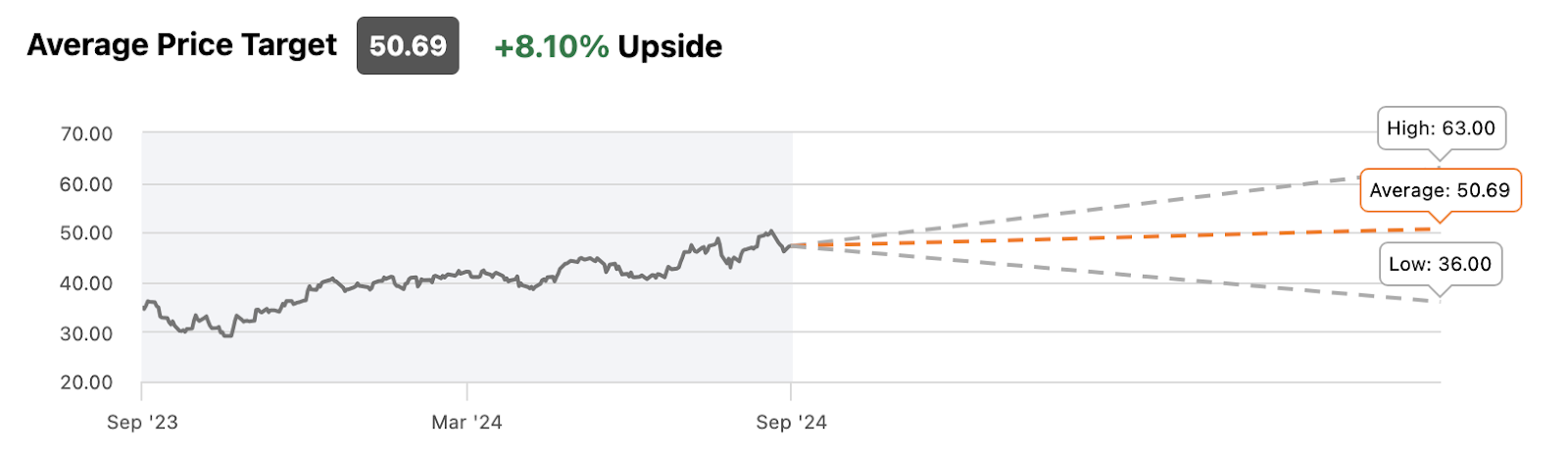

Analyst Perspectives

Wall Street analysts maintain a positive outlook on Brookfield Corporation, with a consensus rating of “Buy.” Price targets range from $36 to $63, with an average target of $50.69, suggesting a potential upside of 8% from current levels.

Source: SeekingAlpha

RBC Capital recently adjusted its price target for Brookfield from $57 to $56 while reiterating an “Outperform” rating. The firm cited Brookfield’s strong fundamentals and significant discount to Net Asset Value (NAV) as key factors behind their optimism.

RBC estimates Brookfield’s shares are currently trading at an 18% discount to NAV, with the company’s real estate portfolio undervalued by as much as 80% compared to its International Financial Reporting Standards (IFRS) fair value. RBC sees this as a clear opportunity for future NAV growth, recognizing Brookfield as one of its top investment ideas due to its diversified portfolio and long-term potential.

Scotiabank also holds a favorable view, maintaining its “Sector Outperform” rating while raising its price target to $51.25 from $50.50. Despite a minor reduction in the 2024 and 2025 distributable earnings estimates, Scotiabank sees Brookfield’s current price levels as an attractive entry point for investors, particularly in light of anticipated Central Bank policy easing.

The firm believes that Brookfield’s strategic communications and positioning could reduce the stock’s discount to NAV, leading to improved returns.

Valuation: A Contrasting View

While analysts remain optimistic, our fair value assessment paints a different picture. Utilizing a combination of valuation models, including Discounted Dividend Model (DDM), EV/Revenue multiples, P/E multiples, and EV/EBITDA multiples, our analysis estimates Brookfield’s fair value at approximately $40 per share.

This represents a potential downside of around 14% from its current trading price, suggesting that the stock may be overvalued relative to its intrinsic value.

Conclusion

Brookfield Corporation has experienced strong gains year-to-date, hitting a 52-week high at the end of August, with solid earnings performance and positive analyst sentiment driving much of its momentum. While price targets from analysts suggest further upside, our fair value models indicate a potential downside risk.

Given these conflicting signals, we believe now may not be the ideal time to invest. It would be prudent to wait for further developments in Brookfield’s strategies before making an investment decision.