Is Canadian Pacific Kansas City Stock a Screaming Buy Right Now?

Canadian Pacific Kansas City; Is Now the Right Time to Buy the Stock?

Canadian Pacific Kansas City Limited (NYSE: CP) stands out as the first and only transnational rail network in North America, connecting Canada, the U.S., and Mexico through a single-line system. The company plays a crucial role in transporting a wide range of goods, including automotive, energy, chemicals, plastics, and industrial products.

In this piece, we’ll explore the company’s recent Q2 earnings report, conduct a fair value assessment, and analyze insights from the options market to evaluate whether CP is a stock worth buying at this point.

Earnings Recap

Canadian Pacific Kansas City Limited (NYSE: CP) delivered a strong Q2 2024 performance, posting a profit of C$1.05 per share, surpassing market expectations of C$1.01 and significantly outpacing last year’s C$0.83 per share. This solid earnings beat underscores the company’s operational resilience and strategic execution, particularly following its transformative merger with Kansas City Southern (KCS).

The company’s revenue also saw a healthy uptick, climbing to $3.603 billion, marking a 13.5% increase over CP’s standalone performance in the same quarter last year. This growth was largely fueled by a substantial $160 million revenue contribution from the recently integrated KCS operations.

On a combined basis, Canadian Pacific Kansas City’s revenue rose by 8% year-over-year, driven by a 6% rise in volume, favorable freight rates, and a $50 million positive impact from foreign currency translation.

Breaking down the performance by segments, the bulk business was a standout, with grain revenues surging by 17% year-over-year, buoyed by strong demand for U.S. grain exports, particularly corn to the Pacific Northwest and Mexico, and soybean and wheat shipments to Mexico. Canadian grain volumes also rose, as farmers began offloading inventories in anticipation of the upcoming harvest season.

Additionally, potash revenues saw a remarkable 24% year-over-year growth, recovering from last year’s lower comparisons due to customer terminal shutdowns. While coal revenues edged up by 3%, U.S. coal volumes dipped slightly, a consequence of lower natural gas prices, though this was partially offset by stronger Canadian coal shipments.

Capitalizing on Synergies and Operational Efficiency

Canadian Pacific Kansas City is currently navigating a period of significant transformation and growth, particularly as it continues to integrate and leverage synergies from the KCS merger. The company’s strategy has focused on optimizing its expansive rail network and improving operational efficiencies, both of which have been instrumental in driving the impressive margin expansion seen in Q2 2024.

The company’s operating margin expanded by an impressive 550 basis points year-over-year, reaching 35.2%. This gain was driven by several factors, including the effective execution of volume growth strategies, improvements in network efficiency, and stringent cost control measures.

Notably, these positive outcomes were achieved despite headwinds such as higher fuel costs, expenses related to the KCS acquisition, and increased spending on purchased services.

Looking ahead, Canadian Pacific Kansas City faces some potential short-term challenges. The company’s margins may come under pressure in Q3 due to anticipated higher casualty expenses, increased stock-based compensation, and the looming risk of labor strikes.

However, these issues are expected to be temporary, with the company well-positioned to resume its positive margin trajectory in the medium to long term. Factors supporting this outlook include continued volume growth, further realization of synergies from the KCS integration, and strategic pricing actions.

The merger with KCS has not only expanded Canadian Pacific Kansas City’s operational footprint but also enhanced its capacity to capitalize on cross-border trade flows, particularly in the context of North America’s evolving trade dynamics. The company is also well-positioned to benefit from broader economic trends such as nearshoring, which is likely to drive increased demand for its rail services.

As Canadian Pacific Kansas City continues to enhance its network efficiency, including faster train speeds and reduced terminal dwell times, it is poised to capture a larger share of the market and deliver sustained growth.

Analysts’ Views

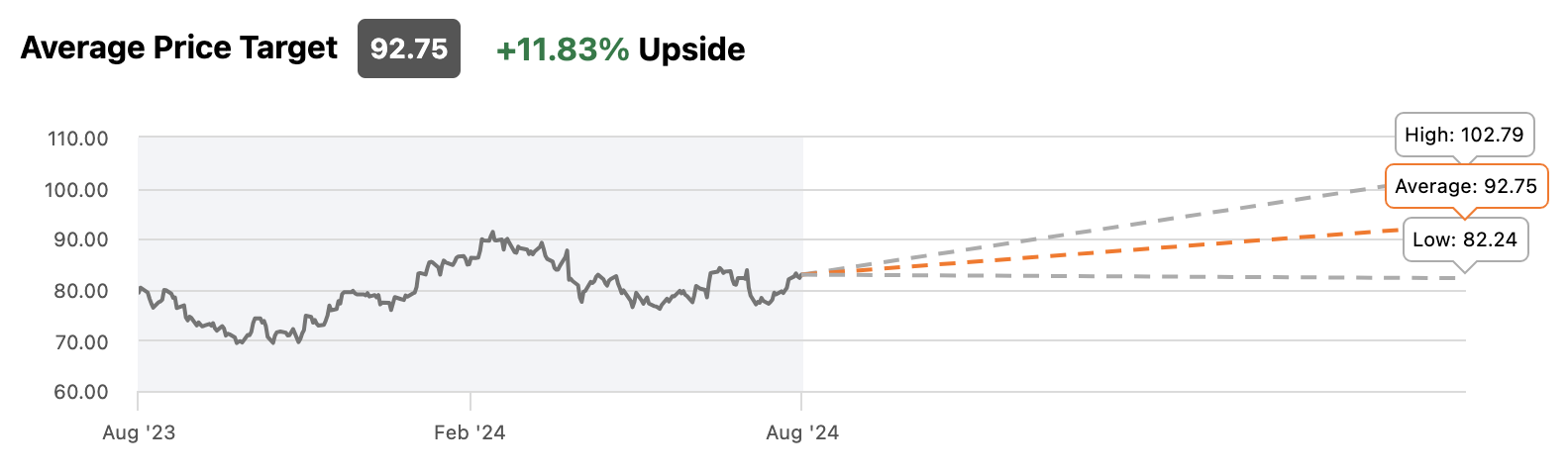

Wall Street analysts maintain an optimistic outlook on Canadian Pacific Kansas City, with an average “Buy” rating. Price targets for the stock range from $82.24 to $102.79, with an average target of $92.75, indicating a potential upside of nearly 12% from current levels.

Source: Seeking Alpha

In recent updates last month, Bernstein raised its price target to $89.06 from $88.50, while maintaining a Market Perform rating. Barclays slightly lowered its target to $95 from $96, reiterating its Overweight rating. Stifel increased its target to $83 from $82, keeping its Hold rating, and Susquehanna maintained a Neutral rating with an $80 price target.

Fair Value Assessment

Our comprehensive fair value assessment of Canadian Pacific Kansas City, utilizing 10 different valuation models including DDM Multi Stage, 5Y DCF Revenue Exit, and EV/EBITDA Multiples, estimates the company’s fair value at approximately $84 per share.

This suggests a potential upside of just around 1% from its current price, indicating that the stock is currently fairly valued. This assessment is slightly less bullish than the views of some Wall Street analysts, suggesting that CP’s stock may be approaching its fair value.

Options Market Sentiment

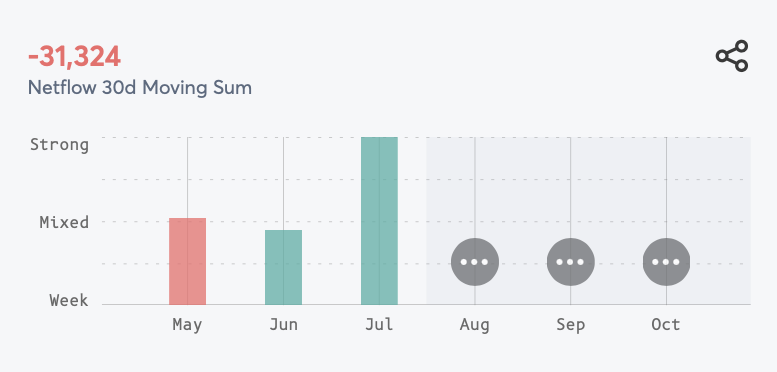

Analyzing options market sentiment provides additional insights into investor expectations. For CP, the -31,324 Netflow 30d Moving Sum indicates a moderate outflow of capital over the past 30 days, reflecting some selling pressure.

The “Mixed” predictions for August, September, and October suggest ongoing market uncertainty, with no clear direction for the stock. This points to potential volatility and price fluctuations in the near term.

Source: Visual Sectors

Conclusion: Hold for Now, Await Q3 Earnings

In summary, Canadian Pacific Kansas City is in a strong position, with solid operational performance and promising growth prospects. However, our fair value analysis indicates that the stock is currently fairly valued, and options market data reflects mixed sentiment over the coming months.

Given these factors, we recommend holding the stock until the next earnings report, expected on October 23, which should provide more clarity on the company’s outlook.