Is Enbridge Stock a Buy, Or a Dividend Trap in 2025?

Assessing Enbridge After Q2 EPS Miss; Is the Stock a Buy?

Earlier this month, Enbridge Inc. (NYSE: ENB), the North American energy infrastructure leader, reported its Q2 earnings, missing EPS consensus estimates. While this might seem concerning at first glance, a more detailed analysis is needed in this case.

In this article, we’ll delve into Enbridge’s recent earnings performance, assess its fair value, and explore market sentiment through options data to determine whether Enbridge is a stock worth considering, even after earnings miss.

Earnings Recap: A Closer Look

Enbridge’s second-quarter earnings report revealed several challenges that have had a significant impact on its financial performance. On August 2, the company reported an EPS of C$0.58, which fell short of Street expectations of C$0.63. A primary factor behind this miss was the substantial downturn in Enbridge’s Canadian Gas Transmission segment.

The segment’s adjusted core profit plunged by 30% to C$98 million year-over-year, which played a crucial role in dragging down the company’s overall results.

The Mainline System, another vital part of Enbridge’s infrastructure, also faced headwinds. Adjusted core profit from the Mainline System decreased by 9.3% to C$1.32 billion.

Despite these setbacks, Enbridge’s management conveyed a more positive outlook during the Q2 2024 Financial Results Conference Call. CEO Greg Ebel expressed confidence in the company’s long-term growth trajectory, driven by strategic advancements and recent acquisitions.

Enbridge raised its 2024 EBITDA guidance to a range of $17.7 billion to $18.3 billion, attributing this uplift to the integration of newly acquired U.S. Gas Utilities. The company also reiterated its commitment to an 8% rate base growth through 2027.

Navigating Challenges and Opportunities

Enbridge’s recent performance highlights the critical need to address weaknesses in its Canadian Gas Transmission segment and to improve the efficiency of the Mainline System. These areas of concern have significantly influenced the company’s ability to meet market expectations.

However, Enbridge’s management has taken proactive steps to enhance its financial outlook. The revised 2024 guidance, which now incorporates contributions from U.S. utilities, exceeded expectations, despite concerns over heavy ATM usage.

This updated guidance suggests that the company is better positioned than initially anticipated, though investors may remain cautious until more comprehensive results are available in 2025, which will include a full-year impact of the U.S. utilities acquisition.

Management’s current strategy emphasizes optimizing existing operations and integrating the U.S. utilities into Enbridge’s broader business model. The company’s $24 billion secured capital program, largely focused on small to medium-sized projects, indicates a deliberate shift away from large-scale M&A activities, which management describes as rare opportunities rather than a strategic norm.

Looking ahead, Enbridge’s expansive footprint in natural gas pipelines and utilities offers a solid foundation for future growth. New developments announced during the quarter are expected to drive higher EBITDA, reinforcing the company’s long-term growth potential. However, the execution of these plans will be crucial in determining whether Enbridge can overcome its current challenges and capitalize on the opportunities.

Analyst Perspectives

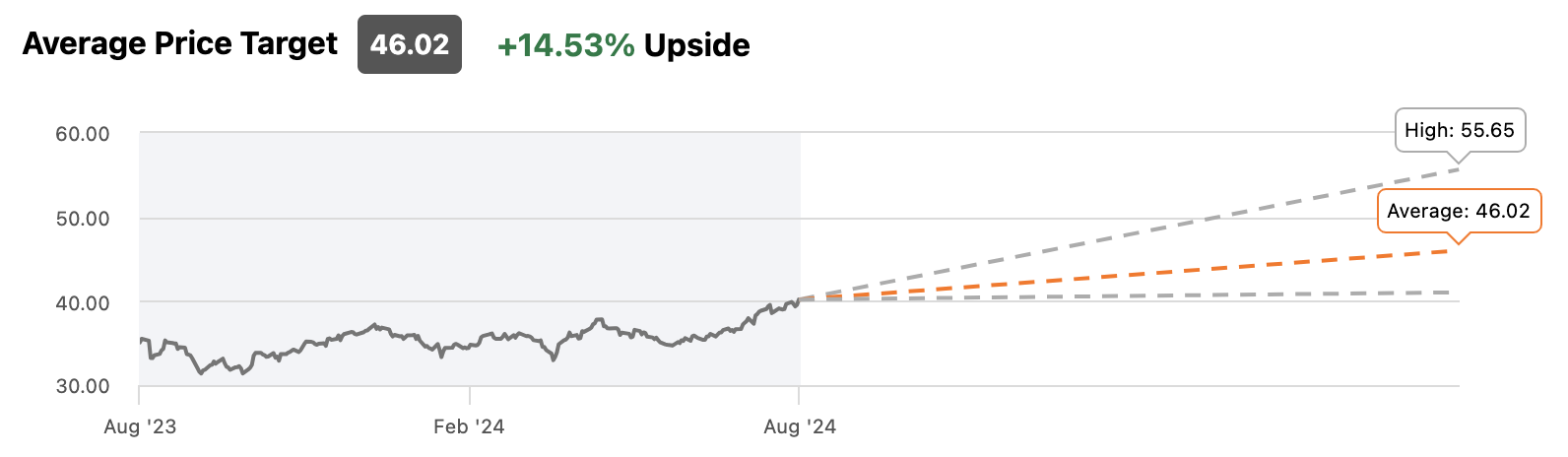

Wall Street analysts remain optimistic about Enbridge’s prospects, with a consensus rating of “Buy.” Price targets for the stock range from $40.94 to $55.65, with an average target of $46.02—indicating a potential upside of 14.53% from current levels.

Source: SeekingAlpha

Valuation

Our fair value analysis, utilizing 14 different models including EV/Revenue Multiples, P/E Multiples, Price/Sales Multiples, and 10Y DCF EBITDA Exit, estimates the fair value of Enbridge’s stock at approximately $33.50 per share. This suggests a potential downside of more than 16% from its current price.

Options Analysis

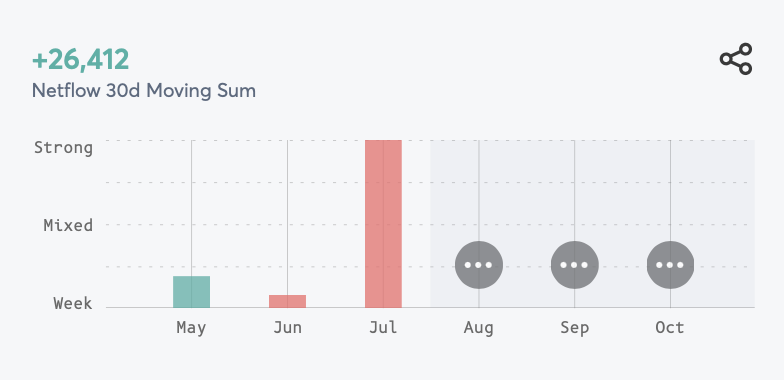

Beyond fundamental analysis, options data provides additional insight into market sentiment. Recent trends show a net positive flow in options contracts, with a 30-day cumulative total of +26,412. However, predictions for August, September, and October are “Mixed,” indicating ongoing market uncertainty with no clear trend. This suggests that the stock may experience volatility and fluctuating prices during this period.

Source: Visual Sectors

Conclusion

In summary, while Enbridge’s recent earnings report shows some areas of concern, the company’s revised 2024 guidance and strategic focus offer some optimism. However, our fair value analysis indicates that the stock is currently overvalued, even as analysts see modest upside potential. Given the mixed signals from options data, it may be prudent to remain on the sidelines until the next earnings report on November 1 provides more clarity.