Loblaw Stock Surges Amid Grocery Market Dominance

Loblaw Companies Limited is a major player in Canada’s retail landscape.

As a leading grocer and pharmacy retailer, Loblaw’s performance often reflects broader economic trends. The company’s ability to navigate these waters speaks to its strong market position and adaptability.

For investors eyeing the Canadian retail sector, Loblaw presents an interesting proposition. Its wide range of stores, from discount to premium, allows it to cater to various consumer segments.

This diversity may provide a buffer against economic fluctuations, making the stock worth a closer look for those seeking stability in their portfolio.

Lets dig into my thoughts below.

Key Takeaways

- Loblaw’s discount factor is fueling growth during an economic downturn

- The company’s diverse store formats cater to a wide range of consumer needs

- Loblaw’s market position in Canada’s retail sector will likely fuel growth moving forward

Earnings – Better than expected as discount stores drive revenue

Loblaw’s recent earnings report shows impressive results, largely driven by its discount store segment.

Revenue increased by 1.5% to $13.9B in the second quarter of 2024.

Adjusted diluted earnings per share rose to $2.15, up 10.8% year-over-year. This beat many analysts’ expectations.

E-commerce sales jumped by 14.2%, showing Loblaw’s digital strategy is paying off. This growth is vital in today’s retail landscape.

The star performers were Loblaw’s discount banners:

- Maxi

- No Frills

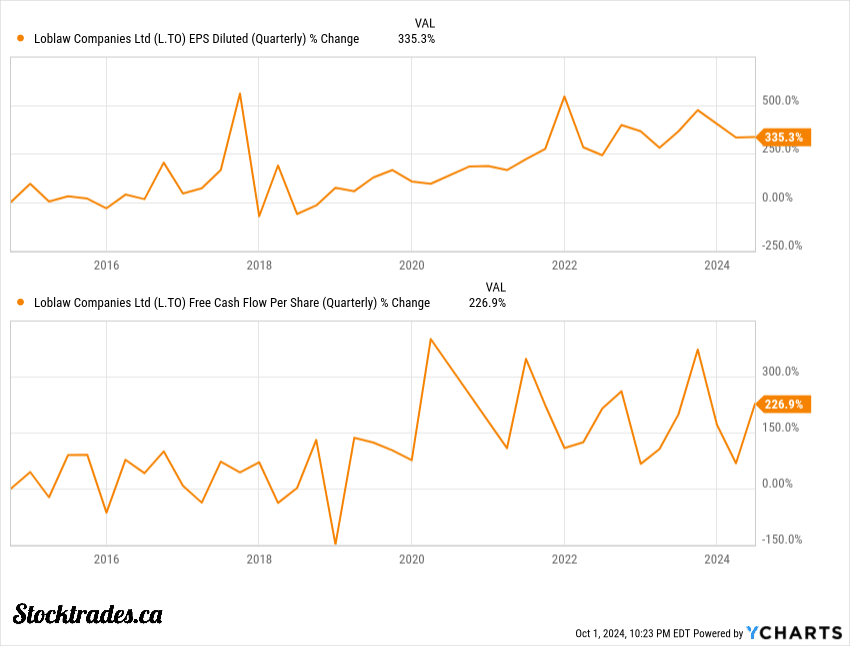

These stores saw strong sales growth as shoppers hunted for bargains. I find this trend telling of the current economic mood in Canada. If you look to the chart below, you can definitely see amplified earnings and free cash flow per share growth in a post-pandemic environment.

Loblaw’s gross profit margin improved by 90 basis points to 32%, and its profit margins remained relatively steady.

Overall, I’m impressed by Loblaw’s performance in a challenging retail environment. The focus on discount offerings and private labels seems to be a winning strategy.

The shift for Canadian consumers is likely permanent, and a tailwind for Loblaw

I believe the changes we’re seeing in Canadian shopping habits are here to stay. Economic pressures have pushed more folks to seek out better deals, and this shift benefits companies like Loblaw.

Canadian consumers are changing their priorities, with value becoming a top concern. This trend isn’t just a blip – it’s a fundamental change in how we shop.

Loblaw’s diverse business model puts it in a prime position to capitalize on this shift. Their discount brands like No Frills and Maxi are attracting more budget-conscious shoppers.

The move to online grocery shopping is another area where Loblaw shines. They’ve invested heavily in their digital platforms, which is paying off as more Canadians embrace e-commerce.

In my view, these factors create a strong tailwinds for Loblaw:

- Growing discount retail segment

- Strong private label brands

- Growing digital presence

As Canadians continue to prioritize value, I expect Loblaw to keep gaining market share.

The company has the widest economic moat out of all Canadian grocers

Loblaw stands out as the grocery chain with the strongest economic moat in Canada. Its massive scale give it a clear edge over competitors like Metro and Sobeys.

On average, every single Canadian is within 10km of a Loblaws store.

One key advantage is Loblaw’s dominant position in both premium and discount segments. This allows the company to capture a wide range of consumers across different income levels.

Loblaw’s private label offerings are another major strength. Brands like President’s Choice and No Name have strong consumer loyalty and higher profit margins than national brands.

The integration of Shoppers Drug Mart into Loblaw’s business has been a game-changer as well. It provides a whole new revenue stream and allows for cross-selling opportunities between grocery and pharmacy.

Its pharmacy segment has been one of the fastest growing segments of the business over the last few years.

In terms of technology and logistics, Loblaw is miles ahead of the competition. Its advanced supply chain and e-commerce capabilities allow for greater efficiencies, thus greater profit margins.

These factors combine to create significant barriers to entry for potential new competitors. The Canadian grocery market is already concentrated, and Loblaw’s wide moat makes it nearly impossible for newcomers to steal market share.

The stock has run up over the last few years, but is it still attractive from a value standpoint?

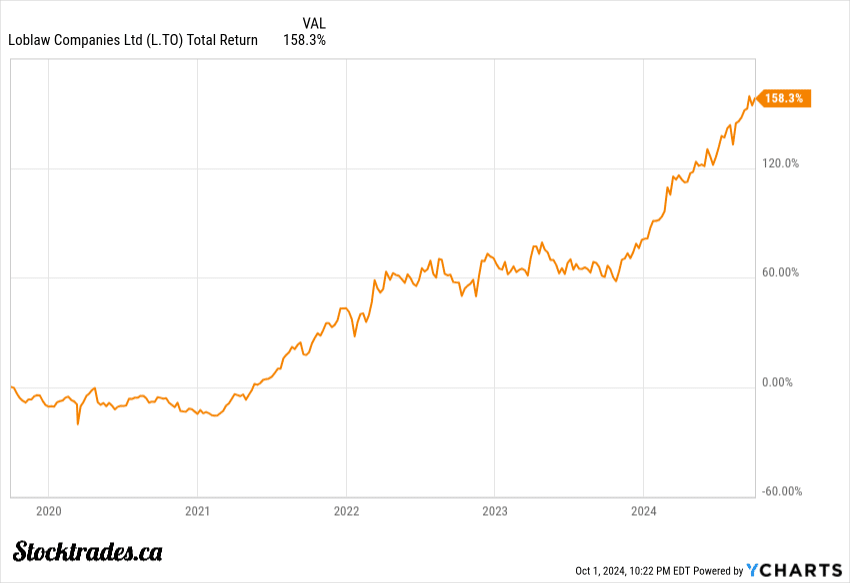

Over the past 5 years, the share price has more than doubled, outpacing not only the TSX but the S&P 500 as well.

Despite this run-up, I believe Loblaw still offers value. Its current P/E ratio of 18 is lower than the Canadian retail sector average of 22.

The company’s dividend yield of 1.1% isn’t particularly high. However, as stock price goes up, yield goes down. I don’t mind a Dividend Aristocrat staying at a low yield, it only means one thing: the stock’s price is going up.

With a payout ratio in the 30% range, I also expect this to continue well into the future.

Loblaw’s long-term growth potential looks strong. The shift towards online grocery shopping and the company’s discount factor amidst a permanent shift in Canadian consumer spending should vault earnings.

Analysts seem to agree on Loblaw’s prospects. The average price target is 15% above the current trading price. Most analysts rate the stock as a “buy” or “strong buy”.

Would I add Loblaw to my portfolio today

As a defensive stock, Loblaw offers stability in uncertain times. This makes many investors believe that it’s a slow-growing, boring stock. The fact it’s outperformed the S&P 500 over the last 5 years has proven that to be dead wrong.

The company’s strong market position in Canadian retail makes it an attractive option for almost all portfolios.

While the current yield isn’t sky-high, I appreciate the company’s track record of steady increases. This signals management’s commitment to shareholder returns, and Loblaw’s free cash flow generation is significant, so shareholders will ultimately continue to reap the benefits.

The stock trades at a reasonable valuation compared to its peers, and although it isn’t the steal you would have gotten when it was $60, don’t make the assumption it’s expensive at $175.

Given its resilient business model and ability to weather economic storms, I maintain a bullish stance on Loblaw stock. While not without risks, I view it as a solid addition to a portfolio, offering reliable earnings growth regardless of the economic circumstances.