Is Pan American Silver (TSE:PAAS) The Best Silver Play in 2024?

In the early part of the year, Wall Street Bets was all the rage. While momentum investing has since cooled, they remain an important community to watch.

One of their targets was silver, which proved far more difficult to manipulate.

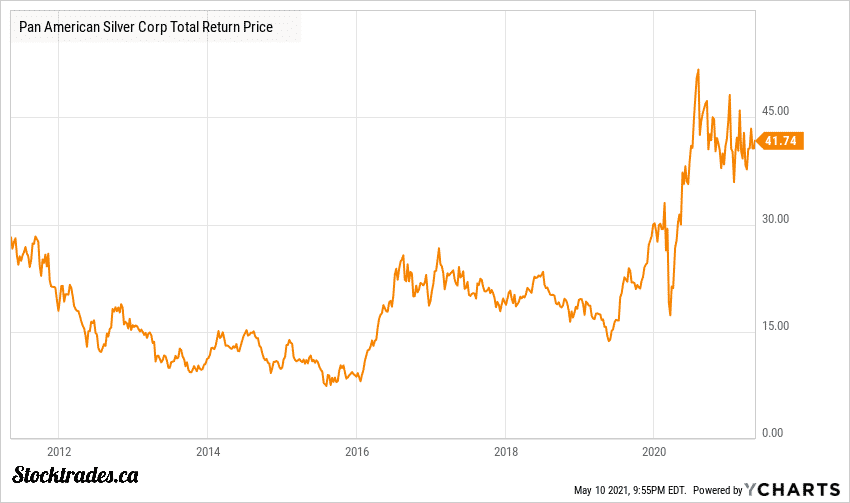

Why silver? While gold has been close to all-time highs, the price of silver is still well below where it was in the early 2010s.

While the gap between silver and gold has been narrowing, it is still sitting at around 66:1 and far above the 30:1 it reached back in 2011.

For those who think silver stocks will outperform gold in the near-to-medium future, than buying Canadian stocks like Pan American Silver (TSE:PAAS) might be worth a look.

What does Pan American Silver (TSE:PAAS) do?

With a market cap just shy of $9B, Pan American is the largest silver stock on the TSX – almost double the size of its closest competitor, First Majestic (TSX:FM).

At 550M oz of silver, it has the largest silver reserves globally. Also worth noting, it has 5.2M oz of gold reserves.

The Canadian stock owns nine producing assets and two in development which are spread out across the Americas. That being said, the company’s assets are primarily based (52%) in Latin America and has operated in the area for 27 years.

Pan American Silver is debt free, a strong sign

As with any miner, I like to look at the company’s financial strength and most importantly, its debt profile. Higher debt profiles can leave miners vulnerable to a correction in the price of metals.

In Pan American’s case, they are well positioned with no long-term debt and having $280M in cash and cash equivalents on the balance sheet.

Pan American is not just a silver pure-play either

It is also worth noting that despite its name, Pan American Silver has recently begun diversifying into gold. In fact, despite having the largest silver reserves in the world, gold is expected to account for 58% of production in fiscal 2021.

Fiscal 2021 guidance calls for record gold production and for silver production to jump by 35% over 2020 levels.

Considering today’s metal prices, Pan American is likely to see strong cash flow generation. Operating cash flow has more than tripled since 2018 and thanks to a growing production base, is on track to once again to generate record cash flows.

What I expect the company to do with those cash flows

In 2020, the company put its cash to good use. First, it wiped out its debt and self-funded the capital expenditures. Secondly, it returned around 31% of free cash flow to shareholders via buybacks (9%) and dividends (23%).

Since the company is debt free, I’d expect the company to balance expansion with returning additional cash to shareholders. The company yields less than 1%, but as we’ve seen across the industry, dividend growth has been ramping up.

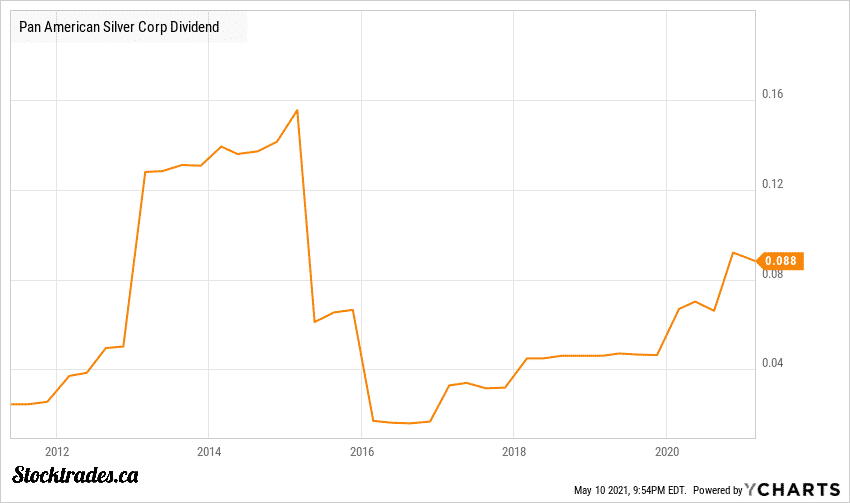

Pan American Silver is in a strong position to grow its dividend

Pan America is sitting on a mini, two-year dividend growth streak over which time it has double the quarterly dividend from $0.035 to $0.07 per share.

Given how well the dividend is covered and so long as metal prices remain strong, the dividend could double again over the next few years.

Worth noting, the company pays the dividend in US dollars which is why the company’s dividend chart might look a little choppy. As the CAD has strengthened against the USD in recent months, it looks like the dividend was ‘cut’ but that is not the case.

That being said, Pan America was among the many miners that slashed the dividend in a material way in the latest precious metal bear market. So, while the current dividend growth is certainly welcomed, caution must be exercised here.

Overall, Pan American looks attractive here thanks to its higher-than-average production growth profile

The company is also trading at a reasonable 14 times forward earnings and for investors looking to benefit from both silver and gold, Pan American is worth another look. Want to see one of the heaviest shorted stocks on the TSX? Have a look at our piece on Dirtt Environmental Solutions Ltd (TSE:DRT).