Is Rogers Communications (TSE:RCI.B) Still a Good Income Option?

I’ve been speaking a lot on telecom stocks recently, so I figured I may as well cap it off with an analysis of Rogers Communications (TSE:RCI.B). Telecoms are excellent Canadian dividend stocks with wide economic moats, and as such they garner a ton of interest from Canadian investors.

If you’re new to buying stocks in Canada, there are three telecoms in particular that form what we call “the Big 3”, and they are Telus (TSE:T), BCE (TSE:BCE), and Rogers.

However, there are some distinct differences between the three in terms of geographical exposure, dividend growth, and stock appreciation.

So with that being said, lets take a look at how Rogers works into the fold in terms of an income option, and what its future growth looks like.

What does Rogers Communication’s (TSE:RCI.B) business model comprise of?

Rogers Communications is currently the third largest telecom company in the country by market cap, at $22.49 billion. The company is also dual listed, trading on the NYSE under the ticker RCI.

The company has service available to over 96% of Canadians and can offer internet speeds of up to 1 Gbps across almost its entire footprint. It has over 25,000 employees country wide and is arguably the most recognized brand in the telecom sector, primarily due to its media exposure.

In 2019, the company generated $15.1 billion in revenue, 61% of that coming from its Wireless segment, 26% from Cable, and the remaining 13% from its Media department.

The company’s wireless segment is clearly fueling growth right now, and it drives revenue through 3 very popular mobility brands, Rogers, Fido, and Chatr.

The company is more prominent in eastern Canada, and officially introduced Canada’s first 5G network.

The expectations for most Canadians owning a big 3 telecom company is sustainable earnings and revenue growth, and an accelerating dividend.

So how has Rogers Communications grown its dividend, and is it safe?

Unfortunately, Rogers decided not to raise the dividend in 2018, instead focusing on debt reduction and expanding infrastructure.

As I mentioned prior, a lot of investors purchase telecom companies for their wide economic moats and strong dividend growth. So as you can expect, the stalling of dividend growth left a sour taste in a lot of investors mouths.

Market Cap: $22.42 billion

Forward P/E: 17.30

Yield: 3.61%

Dividend Growth Streak: 0 years

Payout Ratio (Earnings): 59.00%

Payout Ratio (Free Cash Flows): Premium Members Only

Payout Ratio (Operating Cash Flows): Premium Members Only

1 Yr Div Growth Rate: 4.20%

5 Yr Div Growth Rate: Premium Members Only

Stocktrades Growth Score: Premium Members Only

Stocktrades Dividend Safety Score: Premium Members Only

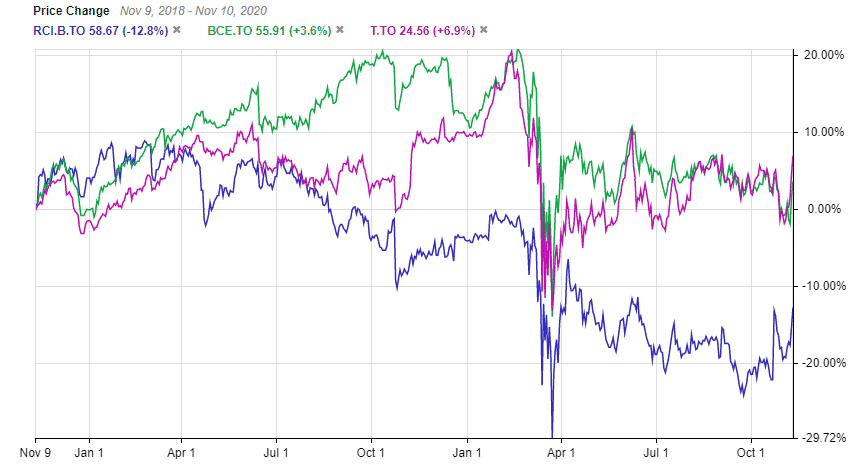

As you can tell from the chart above, Rogers Communications has been the worst performing telecom company in the country by a longshot since 2018.

Although the company has had some struggles elsewhere, you can’t help but think the decision to not raise the dividend and instead focus on capital growth played a part in this underperformance.

However, it’s important we understand the fact that although Rogers did stop dividend growth, it didn’t do so because of lack of capital. The dividend is still safe, and its yield is more than reasonable.

Rogers is currently paying out only 59% of earnings towards the dividend. Compare this to other telecoms like Telus and Bell, who are 100%+, and we can clearly see the dividend is not only safe but also has room to grow.

When we look at the dividend from a free cash flow perspective, which we should always do with telecom companies, it gets even better. Rogers is currently only paying out around 38% of free cash flows towards the dividend.

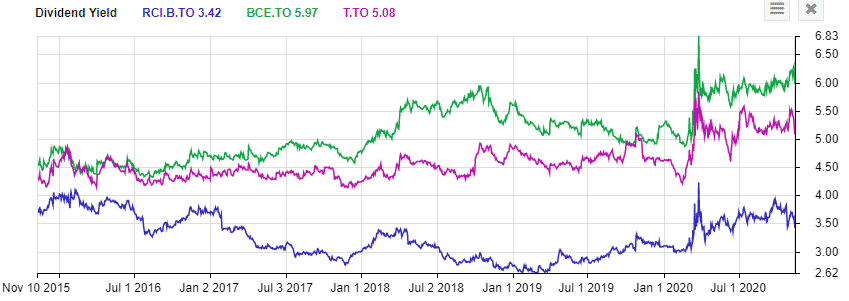

Charts provided by StockRover. Check out Stockrover Here!

At the time of writing, Rogers is yielding around 3.42%, which as you can see by the chart it has been the lowest yielding telecom over the last 5 years. In fact, we can see the gap is getting larger and larger as we move forward.

This is the end result of a company like Telus raising its dividend in the high single digits annually, while Rogers has a 5 year average dividend growth rate of only 1%.

The dividend is safe. In fact, it’s the healthiest dividend out of all 3 major telecoms. However, the lack of dividend growth will make it an unpopular option for Canadian investors moving forward, as I don’t see any of these companies dividends being in danger.

In a situation like that, an investor is likely to choose the one with the higher yield and stronger growth prospects. In my opinion, Rogers holds neither of these.

How will Rogers Communications fuel growth moving forward?

As I’ve mentioned in numerous other articles, these companies struggled to grow over the last while because of rising interest rate environments. Higher interest rates equals more expensive debt. And telecoms have a lot of debt.

So moving forward, we should expect Rogers to generate more bottom line growth just off this alone. But, it’s an equal playing field in this regard. Companies like Telus, BCE, and Cogeco will ultimately benefit much the same.

Shrinking cable growth is often a concern when looking at telecoms these days. It’s an issue in every telecom, and in order to fuel growth, they’ll need to replace that cable revenue and more via internet and wireless subscriptions.

Unfortunately, the company hasn’t been doing that thus far. In fact, Wireless revenue is actually down year over year. If we want to look at numbers prior to the COVID-19 pandemic, revenue in the first quarter of 2020 sat at $2.077 billion, while the first quarter of 2019 was $2.189 billion.

Its media division is taking a big hit due to the pandemic, seeing revenues collapse nearly 50% year over year. This is primarily why I’m a fan of Telus over companies like BCE and Rogers. Where Telus has chosen to expand via security and telehealth, Rogers and BCE’s media divisions are causing a significant drag on earnings right now.

Overall, if you were to ask me in the grand scheme of things if Rogers Communications was a good stock for Canadians to hold, I’d probably say yes.

But, if you were to ask me what my favorite stock in the telecom sector is, I could probably ring off 5 others before I’d consider mentioning Rogers.

It is important to consider the unique characteristics of each company in an industry. Though Canadian telecoms are well liked, each for their various reasons. Just as defensive food stocks are thought to be excelling right now, some like Saputo (TSE:SAP) have struggled.

The stock is undervalued relative to other telecoms right now yes, but its performance also matches the gap in valuations.