Stocktrades Canada

YOU ARE ENTERING A NO-BS INVESTING ZONE FOR CANADIANS

No gimmicky suits, flashy watches, or luxury cars here!

We’re Canadians passionate about making smart financial choices to outpace inflation and retire early. Through years of logic-driven research and insightful opinions, we empower Canadians with trusted, actionable advice.

Self-directed investing can be complex, overwhelming, and stressful. Join over 25,000 investors like you to gain exclusive access to our in-depth research, videos, and insights on top Canadian stocks, ETFs, and investment strategies.

Plus, receive my three game-changing stock picks for 2025 as a bonus!

Canadian Investing Favourites

Our trusted opinions and in-depth research articles have solidified our reputation among Canadians, amassing hundreds of thousands of views annually. These are some of the most comprehensive resources we’ve created, tailored to Canadian investors’ favourite topics.

Dan Kent, Founder of Stocktrades Canada

Growing up around Calgary, Alberta, Dan has been a self-directed for over 16 years, turning his passion for researching stocks into one of Canada’s largest financial websites, Stocktrades, with over 1.4 million visitors in 2024. His insights have been featured in the Globe and Mail, Forbes, Business Insider, CBC, Yahoo Finance, and more. He has also worked with some of the largest financial institutions in the country, like the Bank of Montreal and Toronto Dominion Bank.

Dan co-hosts The Canadian Investor Podcast and runs one of the largest investing communities in Canada, Stocktrades Premium.

With a strong commitment to unbiased, high-quality financial research, Dan built Stocktrades to help Canadians navigate the investing world—without the noise of high fees or click-driven advice of mainstream financial media.

Latest in Canadian Investing

With hundreds of pieces available on the top Canadian stocks or ETFs to buy, you’ll never run out of ideas. Have a look at some of our recently updated or newly published articles below.

Hear trusted feedback from Canadian investors like you!

Join Over 25,000 Canadians Receiving My Insights, Commentary, and Strategies FREE

My jam-packed weekly newsletter will have you in the know about market events, strategies, top stocks, and so much more. All in just a 5 minute read.

Join Our Premium Community

Since 2018, we’ve empowered Canadians with expert research and trusted opinions on top market opportunities. Our Premium platform now supports over 2,000 Canadian investors, helping them invest confidently, boost returns, and achieve early retirement.

Stocktrades Premium

For those who want to identify better stocks

- 52+ In-Depth Market Publications

- Dividend & Growth Buy Lists

- Canadian & US Core Holding Picks

- 6 Strategic Model Portfolios

- 5400+ Stocks Graded Across 90 Core Metrics

- Get Any Question Answered Via My Q&A

- Fully Private Discord

- Full Access To My Portfolio, Transactions, and Returns

- 30-Day Subscription Back Guarantee

Stocktrades ETF Insights

For those who want to identify the best active and passively managed ETFs to add to their portfolios

- Monthly Newsletter Issues

- ETF Shortlists and Best Funds to Buy

- ETF Screener, containing 60+ data points across 5200+ funds

- Get Any Question Answered Via My Q&A

- Fully Private Discord

- Comprehensive case studies and market commentary

- 30-Day Subscription Back Guarantee

Frequently asked questions

With so many investing websites out there these days, I’m sure you have questions about Stock Trades Canada. Let’s answer some of them!

One of the main reasons we started Stocktrades Canada was due to the low-quality content published by mainstream financial media. Most writers on these sites are paid per piece, encouraging quantity over quality. Every piece of content you see here at Stocktrades is produced in-house and by a writer with extensive experience in the financial markets.

Stocktrades.ca was founded in 2016 by investors Daniel Kent and Dylan Callaghan, with the ultimate goal of providing Canadian investors with the best possible tools to increase their investment portfolios. In an industry plagued with misinformation, our main priority is to maintain complete objectivity and bring investors around the world accurate, timely and high quality investment news and information.

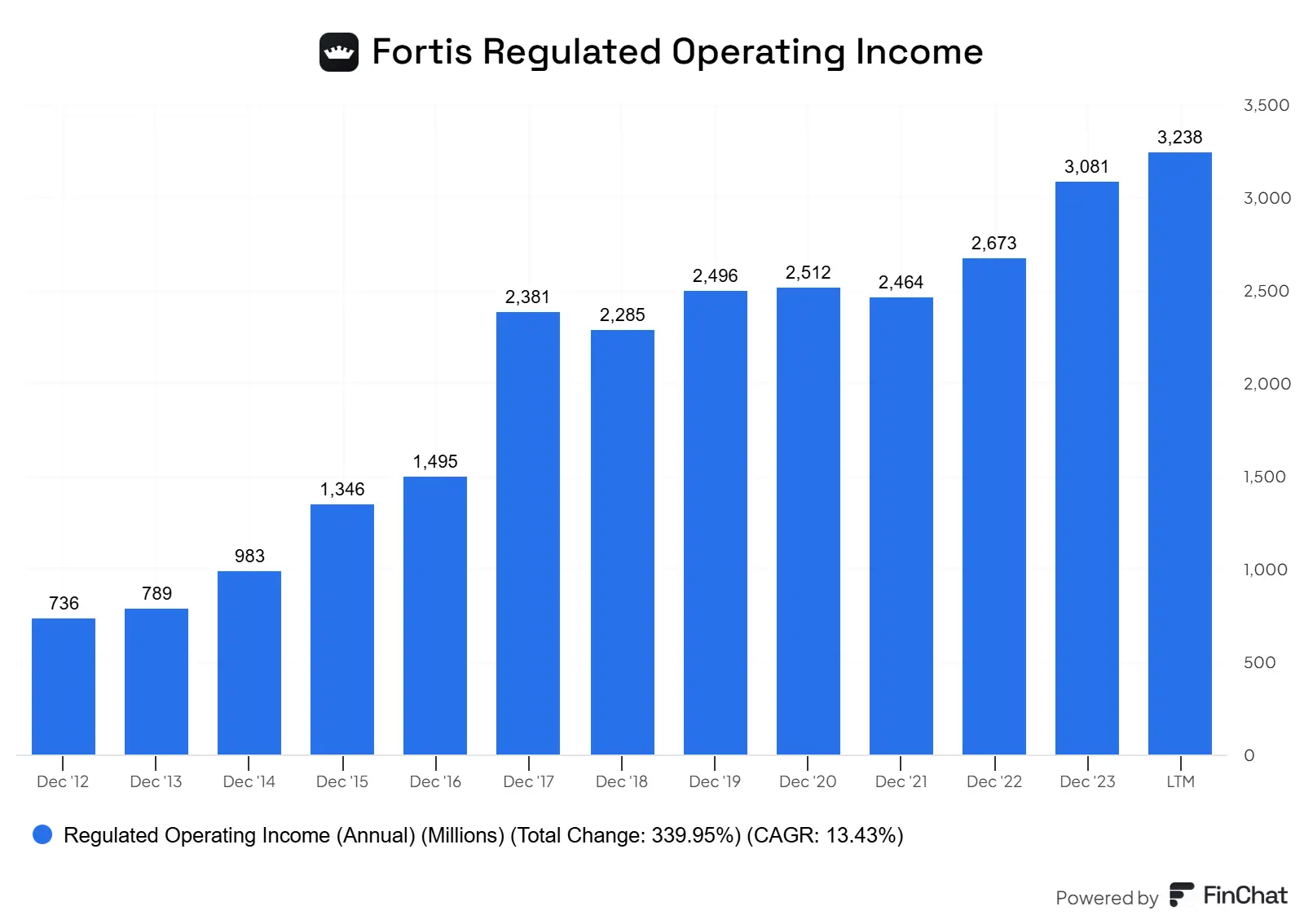

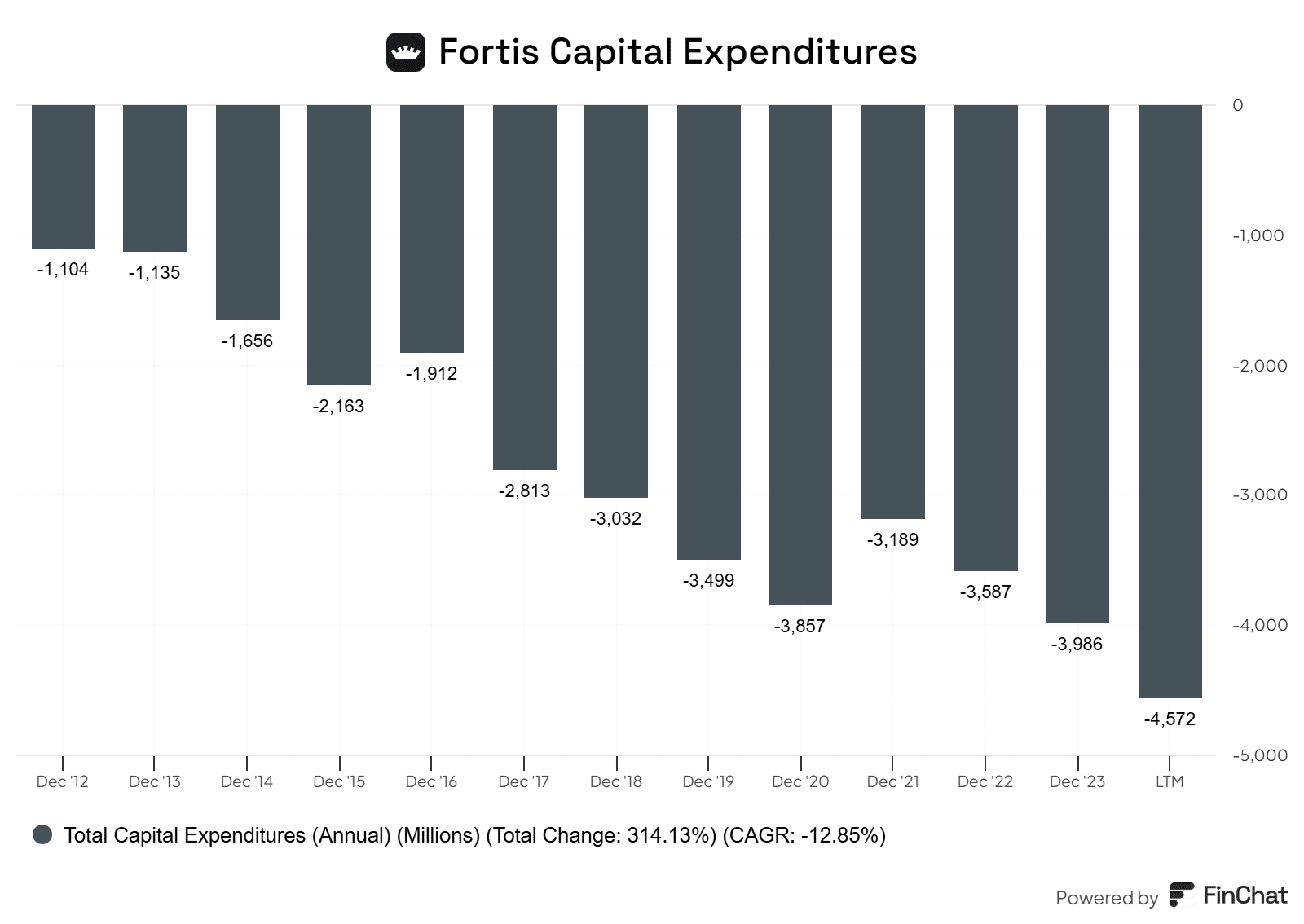

Fortis doesn’t have a lot of key performance indicators to look for. The two primary ones worth keeping an eye on are capital expenditures and regulated operating income. Ultimately more money invested back into the business to grow its asset base is crucial, and in terms of operating income, it gives a picture of the overall health of the underlying business.

Click the images to expand them if needed!

February 14, 2025 – Fortis continues to turn out strong results in a lower-rate environment. Earnings per share of $0.83 topped expectations of $0.81, and the company managed to post mid-single-digit growth in terms of annual earnings per share despite a pretty rocky environment.

Fortis rarely gives me anything to talk about. This is to be expected, as the company generates over 99% of its earnings from regulated utilities. The regulation in utilities makes earnings about as consistent as they can get, and the company rarely ever comes out with any sort of surprises.

On the year, capital expenditures came in at $5.2B. The result of capital expenditures over the last year or so allowed the company’s rate base to increase by 6% on a year-over-year basis. Effectively, the rate base of a utility is what the company utilizes to figure out the pricing it can charge clients for their services. We want to see the rate base continue to grow. With Fortis’s capital plan of $26B invested back into the business from 2025-2029, this should allow it to continue to grow its rate base at a mid-single-digit pace, which should support dividend growth in the same range.

As mentioned, this earnings write-up is relatively short because there isn’t much to talk about. The company’s capital plan should allow it to grow its rate base by 6.5%~ annually through to 2029, which will support mid-single-digit earnings growth and dividend growth. As rates continue to decline, I expect to see more popularity when it comes to Canadian utilities. As a result, we could see valuation multiples continue to expand. In this case, Fortis could put up annual returns over and above its rate base growth.